NS ‘Reaffirms’ Full-Year Adjusted OR Guidance (UPDATED, TD Cowen Insight)

“These results show that our strategy is working and that our momentum is building,” he noted. “We are committed to accomplishing even more in the second half of 2024, and we reaffirm our guidance of a full-year adjusted operating ratio [OR] of approximately 66%.”

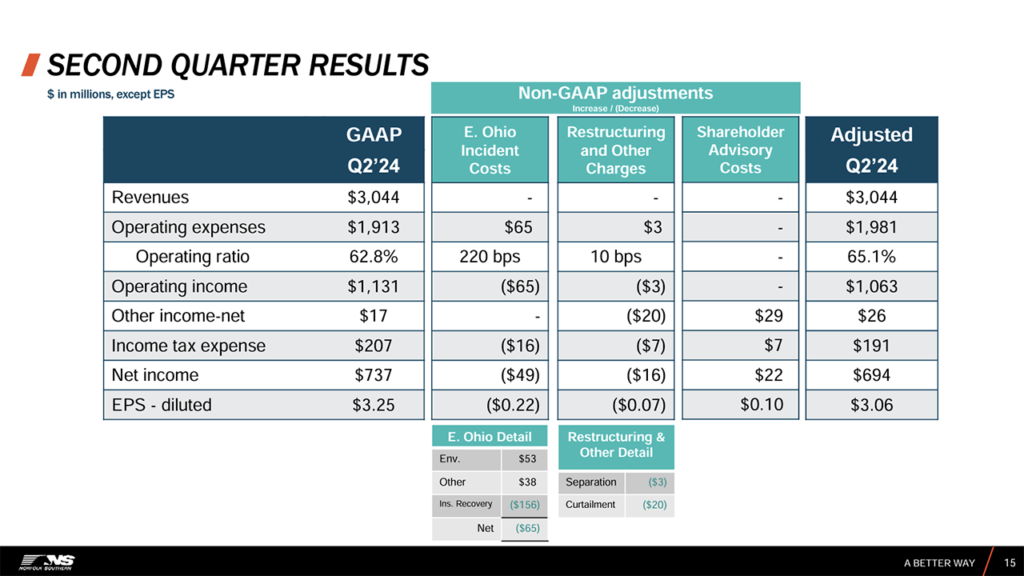

The Class I reported that income from railway operations came in at $1.1 billion, the OR was 62.8%, and diluted earnings per share were $3.25.

After adjusting its results to exclude the impact of the East Palestine, Ohio, derailment, restructuring and other charges, and shareholder advisory costs from the proxy contest, NS said that railway operating income was $1.1 billion, the OR was 65.1%, and diluted earnings per share were $3.06. “Notably, in the second quarter, the impact of the Eastern Ohio incident included insurance recoveries which were greater than the costs incurred in the quarter,” the railroad added.

Due to the East Palestine derailment, NS reported that it “recognized expenses of $527 million and $803 million during the first six months of 2024 and 2023, respectively, for costs related to the incident.” Insurance recoveries “exceeded expenses by $65 million in the second quarter of 2024 compared to expenses of $416 million in the second quarter of 2023,” the railroad noted. “The total expense recognized in the first six months of 2024 includes the impact of $264 million in insurance recoveries, of which $156 million was recognized in the second quarter 2024. No insurance recoveries were recorded during the first six months of 2023. Any additional amounts recoverable under our insurance policies or from third parties will be reflected in future periods in which recovery is considered probable. No amounts have been recorded related to potential third-party recoveries, which may reduce amounts payable by our insurers under applicable insurance coverage.”

Regarding restructuring and other charges, NS reported that during the first six months of 2024, it “executed a voluntary and an involuntary separation program that resulted in a reduction of

approximately 350 management employees.” Charges included $61 million “of costs related to these programs, which primarily consists of separation payments to the impacted management employees.” NS said that it also incurred $35 million of costs associated with the March 2024 appointment of Chief Operating Officer John Orr. Additionally, it said, “‘other income–net’ includes a $20 million curtailment gain on our other post-retirement benefit plan resulting from the restructuring, recorded in the second quarter of 2024.”

As for shareholder advisory costs, “‘other income–net’ includes costs associated with shareholder advisory matters, which amounted to $29 million and $50 million during the second quarter and first six months of 2024, respectively.”

Following are highlights of NS’s second-quarter 2024 results:

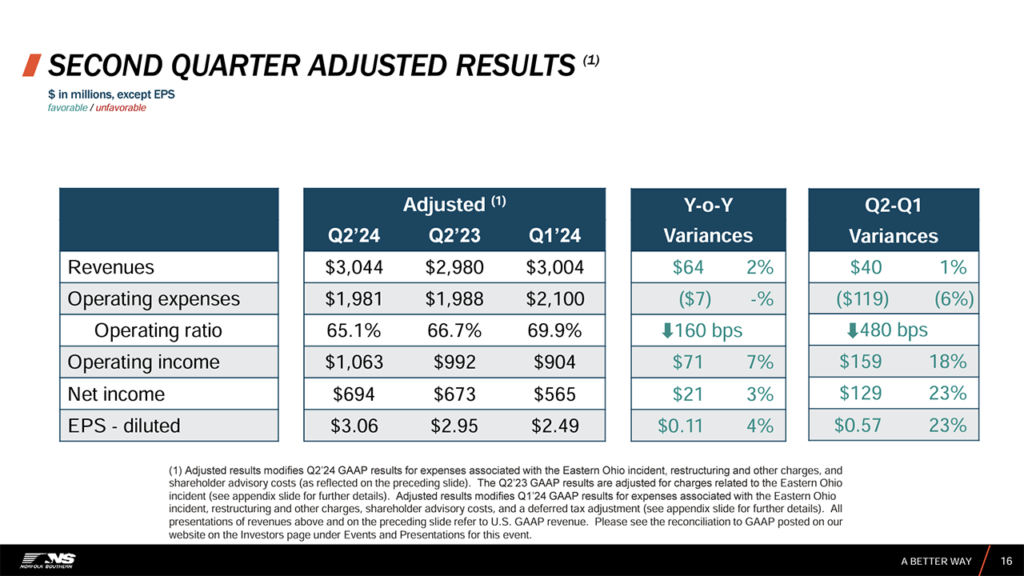

- Railway operating revenues were $3.0 billion, up $64 million, or 2%, compared with second-quarter 2023.

- Income from railway operations came in at $1.1 billion, an increase of $555 million, or 96%, compared with second-quarter 2023. Adjusting for the East Palestine derailment and restructuring and other costs, NS reported that income from railway operations was $1.1 billion, up $71 million, or 7%, compared with the same point last year.

- OR was 62.8% vs. 80.7% in second-quarter 2023. On an adjusted basis, the OR for this year’s second quarter was 65.1%, which NS said represents 160 basis points of improvement from second quarter 2023, which was 66.7%.

- Diluted earnings per share were $3.25, up 108% from second-quarter 2023. Adjusting for the East Palestine derailment, restructuring and other costs, diluted earnings per share were $3.06, up $0.11, or 4%, compared with second-quarter 2023, according to NS.

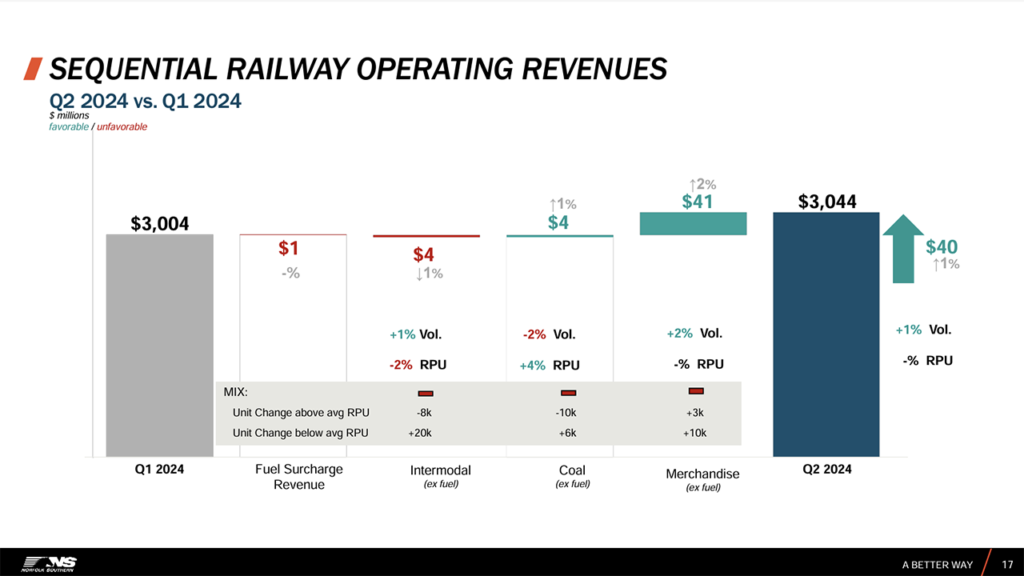

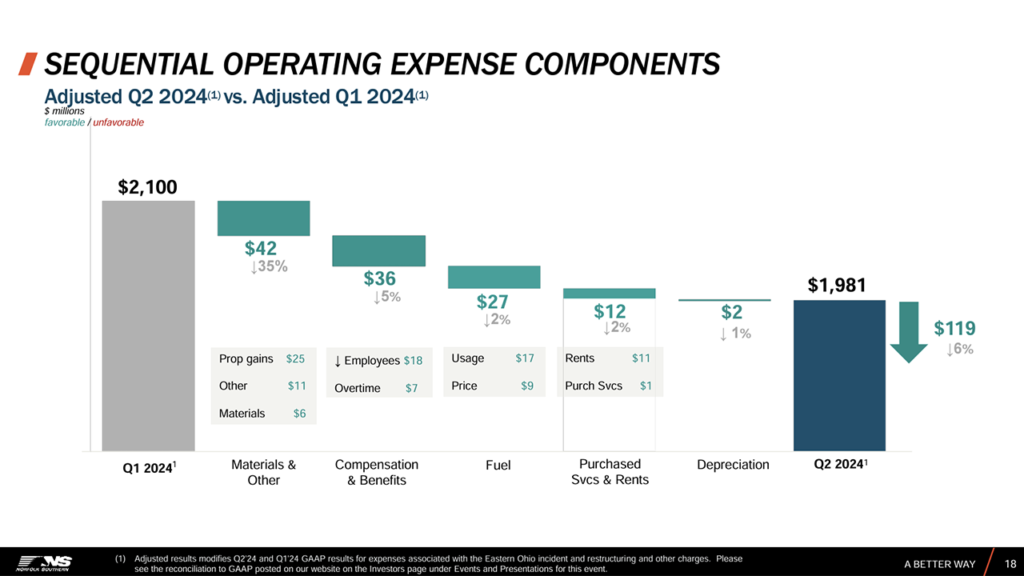

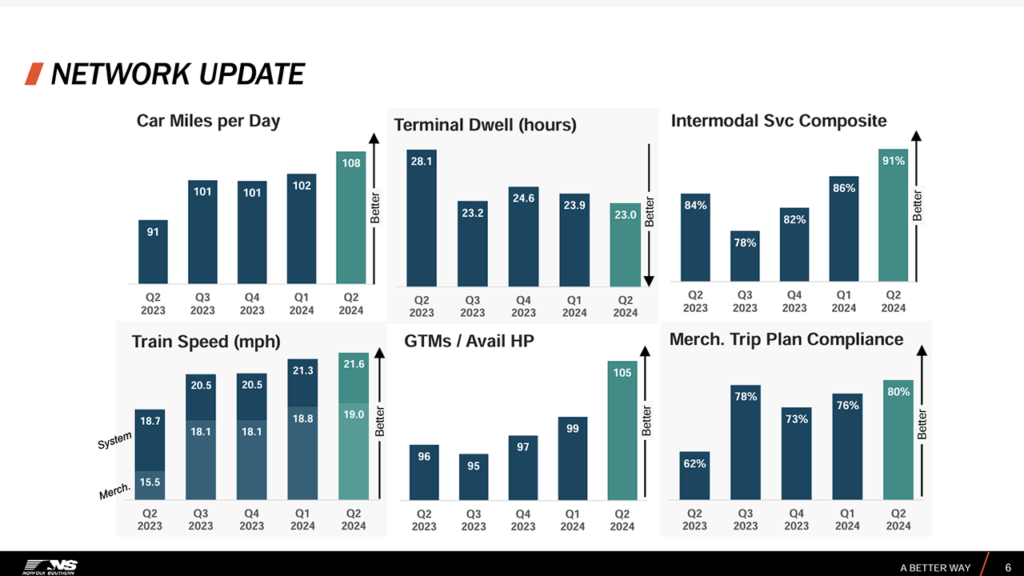

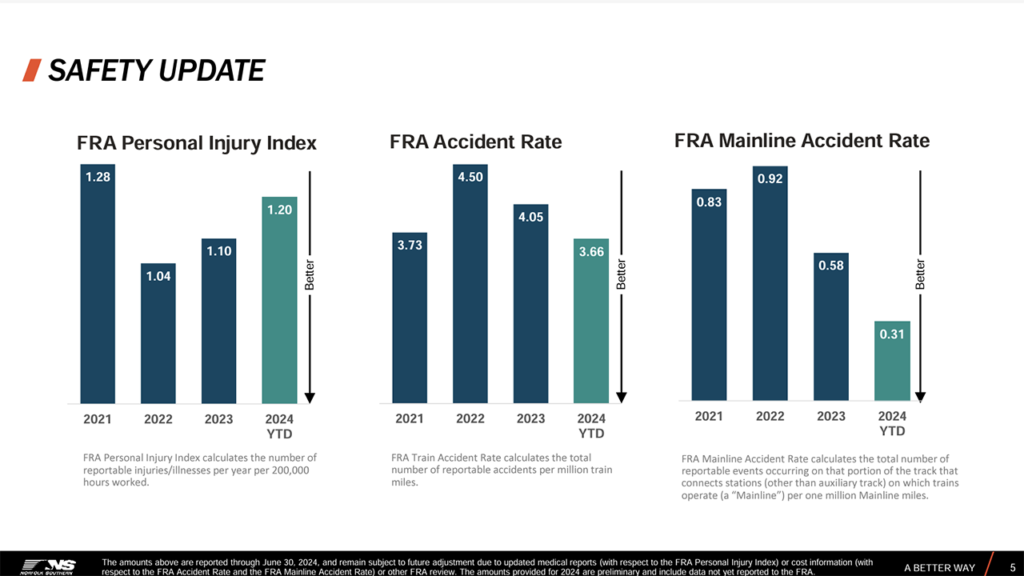

NS also provided a network update and related results. Following are key charts from the Class I’s presentation:

2024 Outlook

NS reported that “meaningful year-on-year margin improvement will be evident as we progress through the year.” It noted that “despite revenue and cost headwinds in the first quarter of 2024, we expect to deliver approximately 400-450 basis points of OR improvement during the second half of 2024.” The railroad said this is consistent with its plan to achieve approximately 100-150 basis points of average annual operating margin improvement, which translates to a 2024 exit ratio of approximately 64%-65%. Additionally, NS said that “despite pressure from lower volume, we remain committed to [the] OR guidance range due to additional cost take out.”

TD COWEN INSIGHT: NS EXHIBITS CONFIDENCE IN ITS PLAN BY MAINTAINING MARGIN GUIDANCE

By Jason Seidl, TD Cowen Managing Director, Industrials and Railway Age Wall Street Contributing Editor

The second quarter came in above our forecast and consensus expectations. Confirmed second-half margin guidance in a tough environment is encouraging as investors (and Street consensus) didn’t expect outlook to hold. The second-quarter margin beat proved targets are achievable though NS still has a lot more wood to chop until freight recovery arrives. Price target to $253; reiterate Hold.

Key TD Cowen Takeaways:

- NSC reported second-quarter adjusted EPS of $3.06 coming in well above our $2.89 estimate and Street forecast of $2.91. Consolidated revenue +2% year over year (y/y) was about in line with our estimates. Adjusted OR of 65.1% beat our estimate by 160 bps as productivity initiatives took hold at the Class I. Second-quarter results exclude impacts from residual East Palestine charges and expenses relating to the proxy battle.

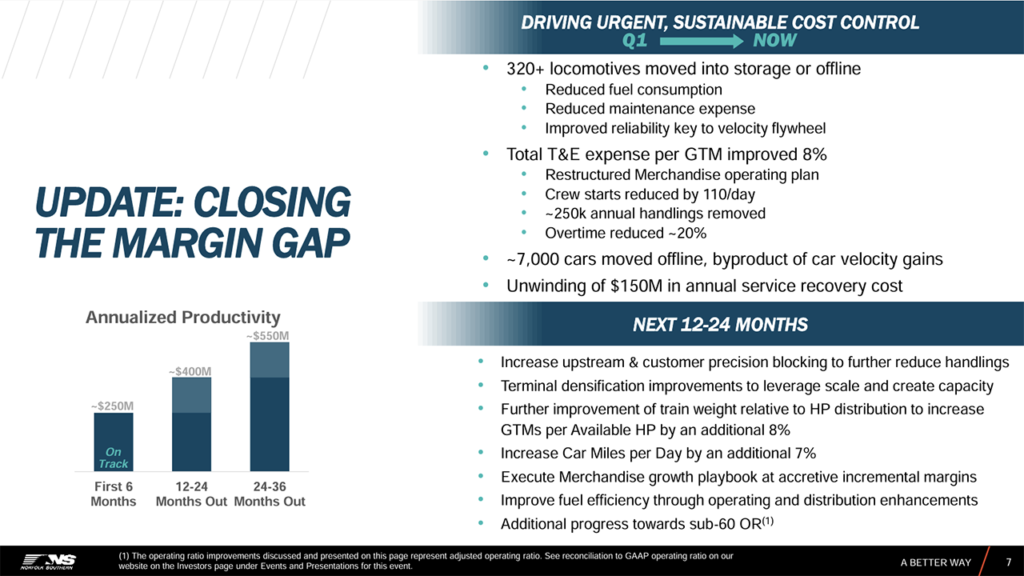

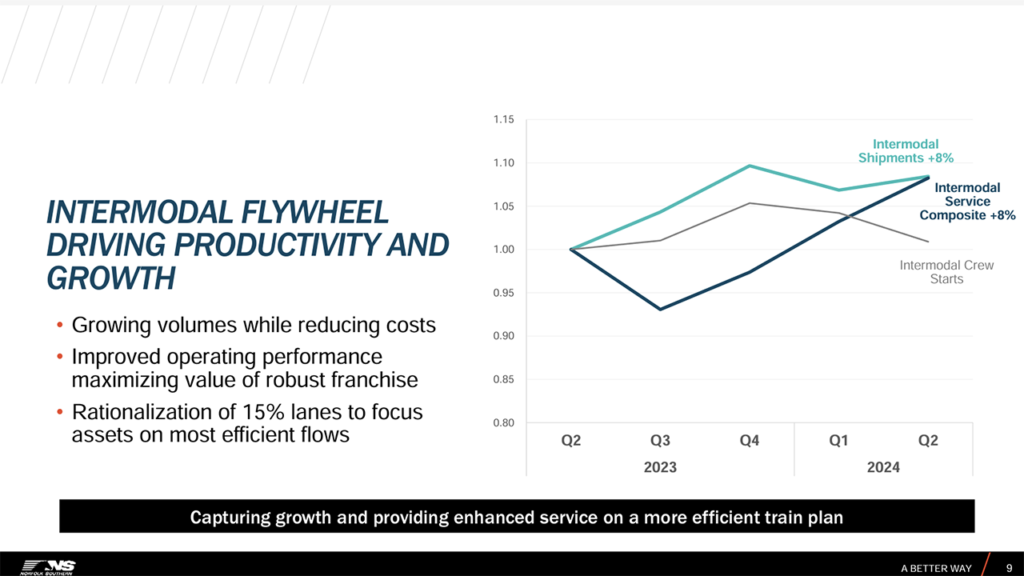

- Costs and the company’s operating plan were the main focus of the call on Thursday [July 25] as NS works to close the gap with peers, NS putting locos into storage (320+), reducing headcount, reducing overtime compensation (though new labor agreements should results in a +$25 million in labor into the third quarter), reducing purchased service needs, among others. NS is pulling approximately 15% of its intermodal lanes out of its network to drive efficiencies; these are smaller and less dense lanes, and shouldn’t reduce productivity even when demand returns. The new operating plan appears to be bearing fruit based on second-quarter results. Indeed, we are encouraged to see NS deliver on its cost initiatives so far; the runway remains long to achieve the 60% target, and we model 225 bps of OR improvement in 2025.

- NS maintained its full year margin targets, which we (and many investors we spoke to going into the print), were not fully confident in, given 1) activist pressure may have led to stretched guidance and 2) guidance had called for material cost takeouts in the second half despite uninspiring volume outlook. NS’s reiterated second-half OR improvement of 400-450 bps, which should put the full year at approximately 66%, and was 50 bps better than the consensus forecast and 40 bps better than our previous estimate. The material second-half margin inflection calls for more costs to come out of the network, despite lowering revenue guidance (from +3% in 2024 to +1%) primarily attributed to weaker pricing and a tepid carloadings outlook.

- Carloads grew 5% y/y in the second quarter driven primarily by intermodal volumes +8% y/y. Like

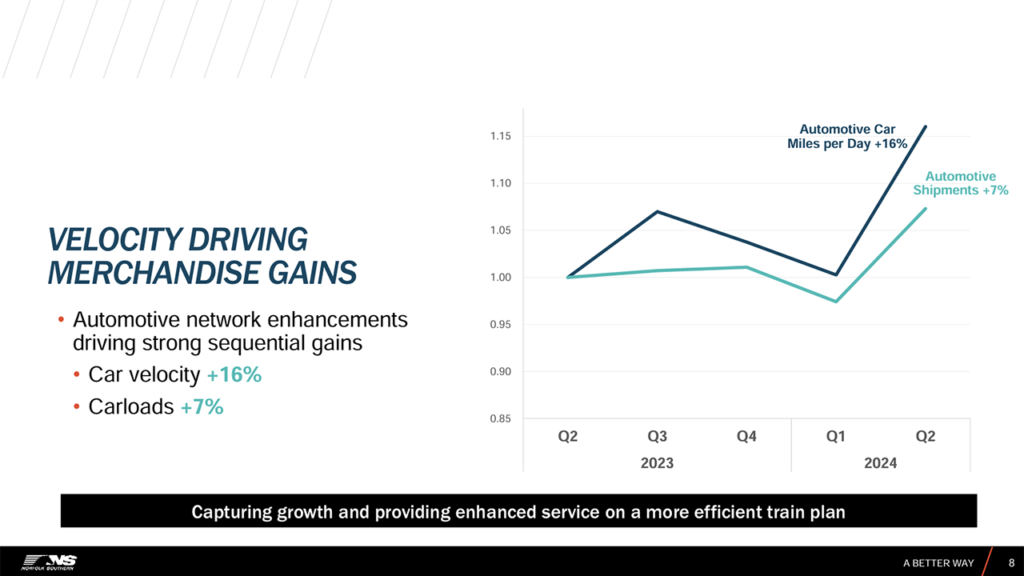

Union Pacific, NS pointed to a softer than expected volume environment developing in the second-half and attributed recent momentum in carloads to improved service metrics with car velocity +6% sequentially and handlings materially reduced in the quarter. NS expects volumes to tick up again in the third quarter but soften in the fourth quarter per typical seasonality. - NS lowered its FY revenue guide to +1% y/y down from +3% y/y on negative mix impacts on yields. Intermodal-driven carload growth is the main driver of the mix effects and NS called out loss of parcel volumes to over-the-road modes and empty container repositioning to the West Coast in addition to some contribution from growth in lower yielding merchandise and autos business. We expect mix pressures to persist into the third quarter just like we assumed for Union Pacific.

- We increase our 2024 and 2025 EPS estimates to $11.90 from $11.75 and $13.65 from $13.55, respectively. Continuing to use our 18.5x multiple and our new 2025 EPS estimate, our price target moves to $253. Reiterate hold.

For more details, visit the NS Investor webpage and/or download the second-quarter 2024 financial documents here:

Further Reading:

- FRA Issues Final Accident Report on NS Derailment

- Spotlight on Safety at NS

- NTSB Issues Final East Palestine Report

- NS Releases Latest Progress Report

- Rail Insights 2024 with NS EVP and COO John Orr – RAIL GROUP ON AIR

- NS Endorses NTSB’s National Safety Policy Recommendations

- NS Confirms 1Q24 Prelim Results, Outlines Strategy (UPDATED, 4/25)

- NS 1Q24 Prelim Results Reflect East Palestine Settlement (Updated Following NYSE Close)