So it was, following a dark night highway-rail grade crossing accident, that the train’s conductor swore under oath he was waving a lantern “back and forth” prior to the automobile operator ignoring the lantern and driving onto the tracks in front of the locomotive. The case is decided in favor of the railroad, with the conductor later commenting to the railroad attorney, “I’m glad I wasn’t asked if the lantern was lighted.” And so it is that there are truths and whole truths.

Upon being appointed Surface Transportation Board (STB) chairperson by POTUS 47 on Jan. 20, 2025, Republican Patrick J. Fuchs, with unanimous peer support, promised an agency providing the public with whole truths. He later told Railway Age his focus was “getting all the facts and elevating transparency in agency decision making.”

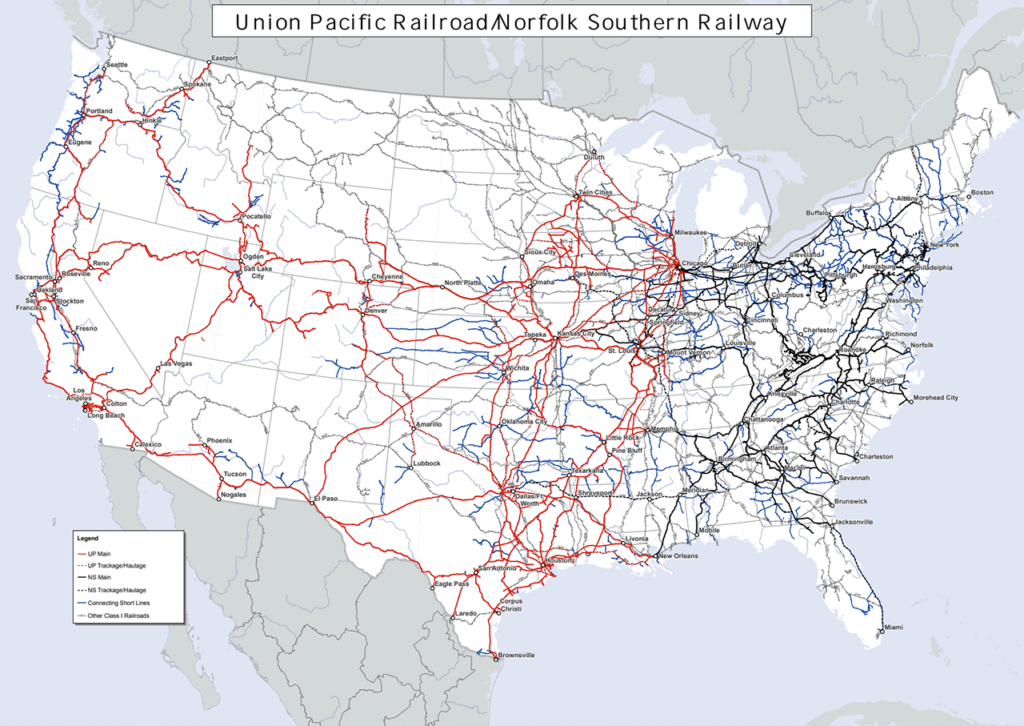

That unanimous bipartisan commitment to tell-it-all was extended by a March 18 STB decision (Docket F.D. 36873; download below) directed at Union Pacific (UP) and Norfolk Southern (NS), who are expected by April 30 to file a merger application to create the first U.S. Atlantic-to-Pacific railroad. The STB is requiring of UP and NS the same full disclosure—whole truths—as the Department of Justice (DOJ), under provisions of the Hart-Scott-Rodino Act, requires of non-railroad merger applicants.

Although the STB has exclusive statutory authority to approve or disapprove railroad mergers, and impose conditions, DOJ may elect to file comments, which the Board considers along with those of other parties.

The STB’s March 18 order follows a March 3 letter from DOJ’s Antitrust Division urging the Board to compel UP and NS to provide, ahead of their April 30-expected merger application, “relevant ordinary course documents.” DOJ identifies them as transaction documents analyzing markets, market shares, competition, competitors, entry into new markets and synergies.

The STB, quoting from DOJ’s letter, said while the Hart-Scott-Rodino Act does not apply to Board proceedings, “access to such documents [which STB otherwise has authority to compel] is imperative in evaluating the potential anticompetitive effects of a proposed merger” and will “ensure a robust record for the Board’s decision making.”

The STB gave UP and NS until April 7 to provide the relevant documents such as produced in-house and by outside advisors. This gives the Board some three weeks to review them prior to UP and NS refiling a merger application—a prior one having been rejected Jan. 16 as “incomplete” (without prejudice to refiling). Should the STB accept a refiled application within a 30-day review period, it will set a procedural schedule, including public and stakeholder comment periods, with a decision expected within 12-15 months.

Although UP and NS responded they “are not refusing” to produce such documents and would “conduct reasonable searches,” they raised concern over producing “highly sensitive internal company documents.”

The concern may be that the documents sought may conflict with documents merger applicants typically provide the Board. When predicting future events, conflicting estimates are common, but it is data most beneficial to the desired outcome that is supplied.

To this concern, the Board said that while some of the sought documents may be “highly sensitive,” applicants may designate them “confidential” or “highly confidential” and they would be shielded by a protective order.

The STB said it is “appropriate” to demand these documents “given the proposed transaction’s size and significance, and because the transaction is the first to be assessed under the 2001 merger rules. Moreover, the Board finds that these documents will assist it in determining whether the proposed transaction is likely to have the effects attributed to it by applicants and whether the transaction is consistent with the public interest”—truths vs. whole truths.

The documents sought, said the STB, “are likely to provide valuable insight into the proposed transaction’s effects because they reflect real-time business decisions and forecasts concerning the merging parties’ operations, and views of past, present and future market conditions [and] may be more probative … than self-serving statements’ provided to support a merger application.”

Although this unanimous decision of three Board members—Fuchs, fellow Republican Michelle A. Schultz and Democrat Karen J. Hedlund—was silent on the source, it clearly reflects in tone and substance former President Ronald Reagan—“trust, but verify.”

Railway Age Capitol Hill Contributing Editor Frank N. Wilner is author of “Railroads & Economic Regulation,” available from Simmons-Boardman Books, 800-228-9670.