The cost of capital represents the STB Office of Economics’ estimate of the average rate of return needed to persuade investors to provide capital to the industry, according to the STB’s Aug. 6 decision (download below). The cost of capital was 10.58% in 2022, 10.37% in 2021, and 7.89% in 2020.

Calculated annually, the cost of capital is an aggregate measure and “not intended to measure the desirability of any individual capital investment project”; it “is one component used in evaluating the adequacy of a railroad’s revenue each year … [and] may also be used in other regulatory proceedings, including (but not limited to) those involving the prescription of maximum reasonable rate levels, the proposed abandonment of rail lines, and the setting of compensation for use of another carrier’s lines,” STB explained.

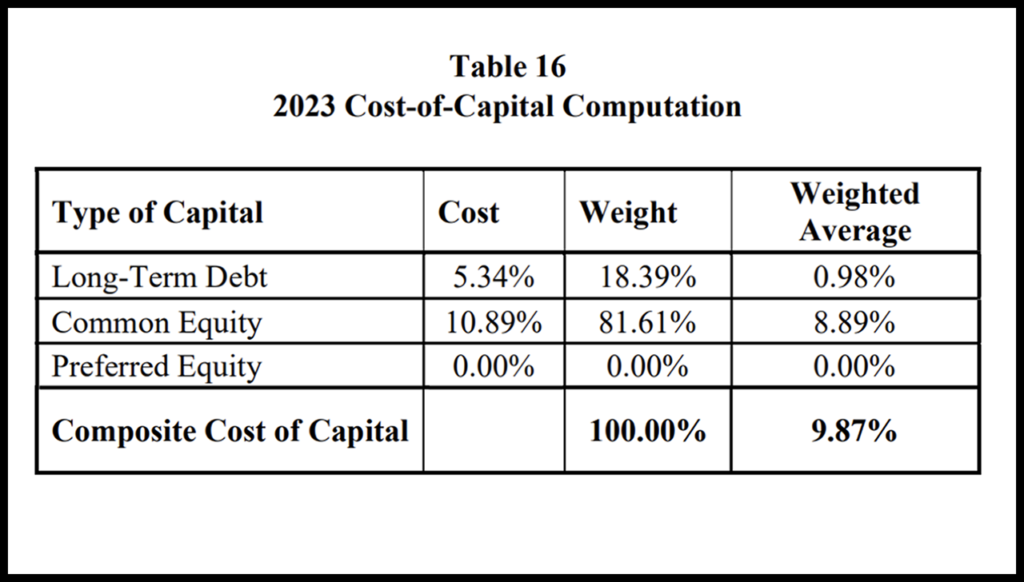

The federal agency reported that for 2023:

- The cost of railroad long-term debt was 5.34% (vs. 4.28% in 2022, 2.63% in 2021, and 2.54% in 2020).

- The cost of common equity was 10.89% (compared with 11.99 in 2022, 12.03% in 2021, and 9.33% in 2020).

- The cost of preferred equity was 0% (vs. 0% in 2022, 0% in 2021, and 3.42% in 2020).

- The capital structure mix of the railroads was 18.39% long-term debt (vs. 18.28% in 2022, 17.71% in 2021, and 21.16% in 2020); 81.61% common equity (vs. 81.72% in 2022, 82.29% in 2021, and 78.84% in 2020); and 0.00% preferred equity (vs. 0.00% in 2022, 0.00% for 2021, and 0.00% for 2020).

“This proceeding was instituted by decision served on February 20, 2024, to update the railroad industry’s cost of capital for 2023,” the STB reported. “In that decision, the Board solicited comments from interested parties on the following issues: (1) the railroads’ 2023 current cost of debt capital, (2) the railroads’ 2023 current cost of preferred equity capital (if any), (3) the railroads’ 2023 cost of common equity capital, and (4) the 2023 capital structure mix of the railroad industry on a market value basis. The Board received comments from the Association of American Railroads (AAR) providing the information used to calculate the annual cost-of-capital determination, as established in Use of a Multi-Stage Discounted Cash Flow Model in Determining the Railroad Industry’s Cost of Capital, EP 664 (Sub-No. 1).”

“Western Coal Traffic League (WCTL) replied to AAR’s submission, stating that its review of AAR’s filing and associated workpapers did not reveal any significant mathematical errors,” the STB said. “Nevertheless, WCTL argues that the cost of capital is substantially overstated due to a miscalculation of the cost of equity, which stems from alleged flaws in the Multi-Stage Discounted Cash Flow model (MSDCF), and argues for the implementation of the Capital Asset Pricing Model (CAPM). As in previous years, WCTL recommends the Board rely only on CAPM, but with a 4.6% market-risk premium, to calculate the cost-of-equity portion of the cost of capital … AAR responded to WCTL’s reply, asserting that it followed the Board’s instructions to use the methodology from Railroad Cost of Capital––2022, EP 558 (Sub-No. 26) …, and noting that WCTL acknowledges that AAR’s filing and associated workpapers had no significant mathematical errors … AAR asserts that WCTL’s arguments are collateral attacks on the Board’s cost-of-capital methodology and should therefore be rejected.”

According to the STB, “WCTL argues that AAR’s cost-of-equity calculation ‘deviates substantially’ from other respected benchmarks because the Board miscalculates the cost of equity due to alleged flaws in the Board’s methodology … WCTL also contests certain MSDCF data inputs and the sources used to calculate earnings per share growth rates …”

As in previous years, “WCTL presents alternative cost-of-capital figures—this year ranging from 7.04% to 8%,” the STB reported. “WCTL uses a variety of alternative methods and critiques the MSDCF while supporting the CAPM-only approach and its calculation of the cost of equity. As WCTL recognizes, the Board is not under an ‘immediate legal obligation to consider such matters in this particular proceeding’ … Nevertheless, WCTL argues that the deviation between the cost-of-capital values derived by the Board and the values it presents “is more than worthy of a Board-initiated rulemaking proceeding” … The Board has previously directed in past annual cost-of-capital proceedings that challenges to the Board’s cost-of-capital methodology should be addressed in Docket No. EP 664 and not in the annual cost-of-capital proceeding … As the Board has stated, ‘requests to [change our methodology] must be brought (in the form of a petition for rulemaking) in a 664 proceeding, not in the annual 558 proceeding, in which we calculate the cost of capital for a particular year’ … As WCTL appears to concede, … its arguments are challenges to the Board’s methodology. Accordingly, they are not properly before the Board in this annual proceeding and are not being considered at this time. The Board will accept AAR’s submission, which complies with the Board’s established methodology.”