Merchandise and Intermodal revenue and volume growth, partially offset by a decline in coal and other factors, characterized CSX’s second-quarter and first-half performance. The railroad is embarking on an all-encompassing safety improvement program led by its Operations and Safety teams.

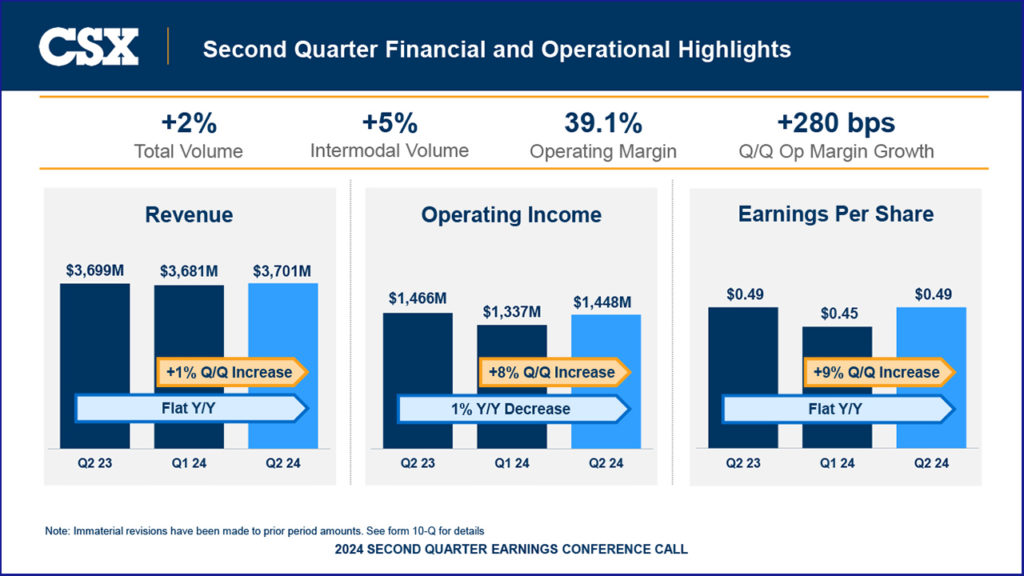

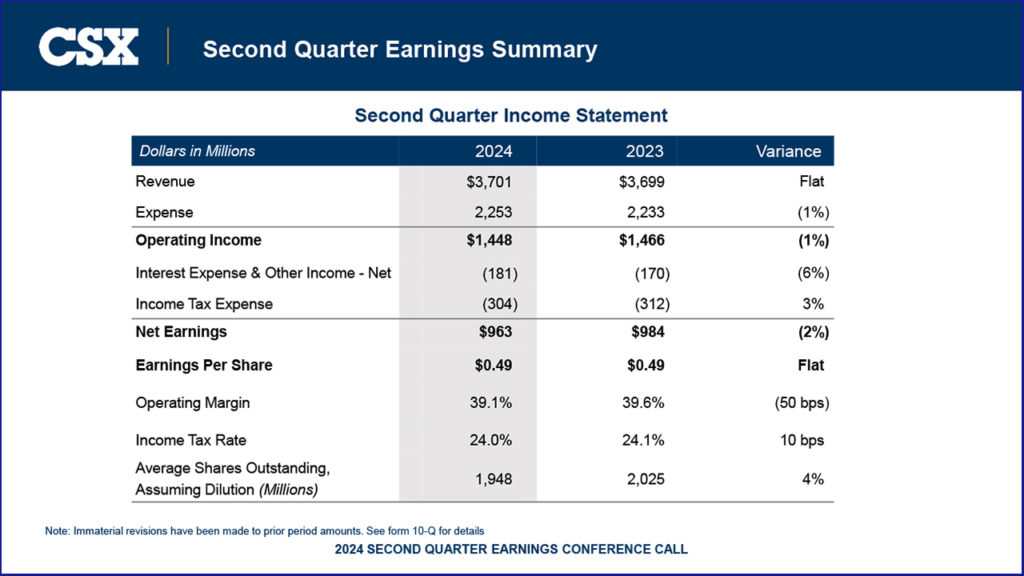

CSX reported 2Q24 operating income of $1.45 billion compared to $1.47 billion in the prior year period. Net earnings were $963 million, or $0.49 per diluted share, compared to $984 million, or $0.49 per diluted share, in the same period last year. Total volume of 1.58 million units for the quarter was 2% higher compared to 2Q23.

Second Quarter Financial Highlights

- Revenue totaled $3.70 billion for the quarter, which was flat year-over-year as the positive effects of merchandise pricing gains and growth in intermodal and merchandise volume were offset by declines in export coal prices, a reduction in other revenue and lower fuel surcharge.

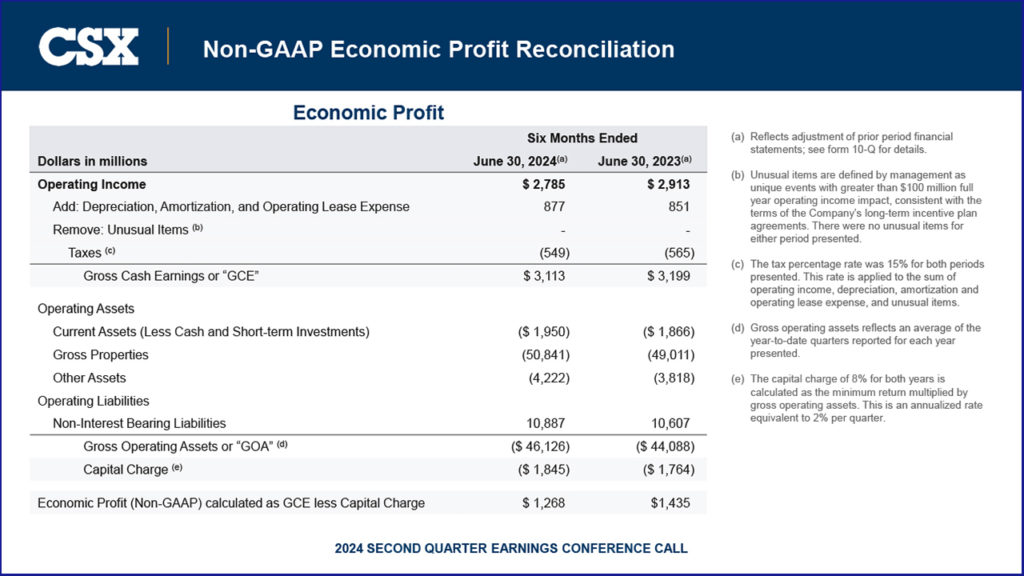

- Operating income of $1.45 billion decreased 1% compared to the same period in 2023 while increasing 8% from 1Q24. CSX’s 2Q24 operating ratio was 60.9% (CSX called it a ”39.1% Operating Margin”), increasing 50 basis points year-over-year but decreasing 280 basis points sequentially.

- Diluted EPS of $0.49 was flat compared to the prior year but increased 9% compared to the previous quarter.

“CSX remained focused on efficiently serving our customers over the second quarter, allowing us to deliver strong sequential increases in volume, operating income, margin, and earnings per share,” said President and CEO Joe Hinrichs. “I am proud of our railroad’s performance, including our team’s effective response to the disruptions at the Port of Baltimore. As we continue to execute through shifting markets, CSX is well-positioned to achieve solid year-over-year margin expansion over the remainder of 2024.”

“We’re working hard to be the railroad we know we can be,” Hinrichs told Railway Age. ”We’ve made a lot of progress, but there’s a lot more to be accomplished.”

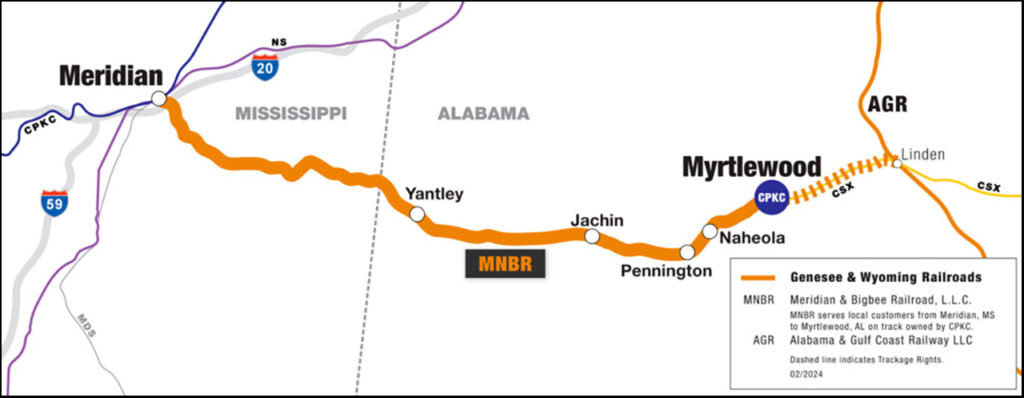

CSX’s 2024 capex program will total approximately $2.5 billion, consisting of safety investments, capacity and equipment additions, technology enhancements, the MNBR (Genesee & Wyoming Class III Meridian & Bigbee) interchange at Montgomery, Ala., and “high-return growth projects,” Hinrichs said. CSX has “a balanced approach to capital returns.”

Safety-wise, CSX Executive Vice President and Chief Operating Officer Mike Cory said the FRA reportable injury rate, which increased slightly from 1.20 in 1Q24 to 1.25 in 2Q24, “is a key area of focus.” The FRA train accident rate dropped dramatically, from 4.09 in 1Q24 to 2.62, “as CSX fosters a fundamental safety culture centered on effective mentorship.” The company is launching “an extensive, three-year program aimed at strengthening our safety leadership skills and building employee engagement,” Cory noted.

The safety initiative, led by Mike Cory and the Operations team and Vice President and Chief Safety Officer Jim Schwichtenberg and his group, will be assisted by DEKRA North America, described as “the world’s largest independent, non-listed expert organization in the field of testing, inspection and certification.” The program, which includes classroom and onsite instruction, “will touch every employee in our 26-state, two-Canadian-province network,” Hinrichs told Railway Age. “It’s based on self-awareness, identifying and reducing risk. As an industry, railroads have way too many personal injuries and accidents. We accept and tolerate risk more than we should. Like many other industries did years ago, our industry needs to step back and take a hard look at itself, and identify ways we can educate our people that this is not acceptable. At CSX, we’ve been focusing on train accidents, which are high-risk and largely caused by human error. Our FRA numbers show that. Now, it’s time to turn our attention to things like slips, trips and falls and employee transport accidents. Our union leaders are on board with this program.”

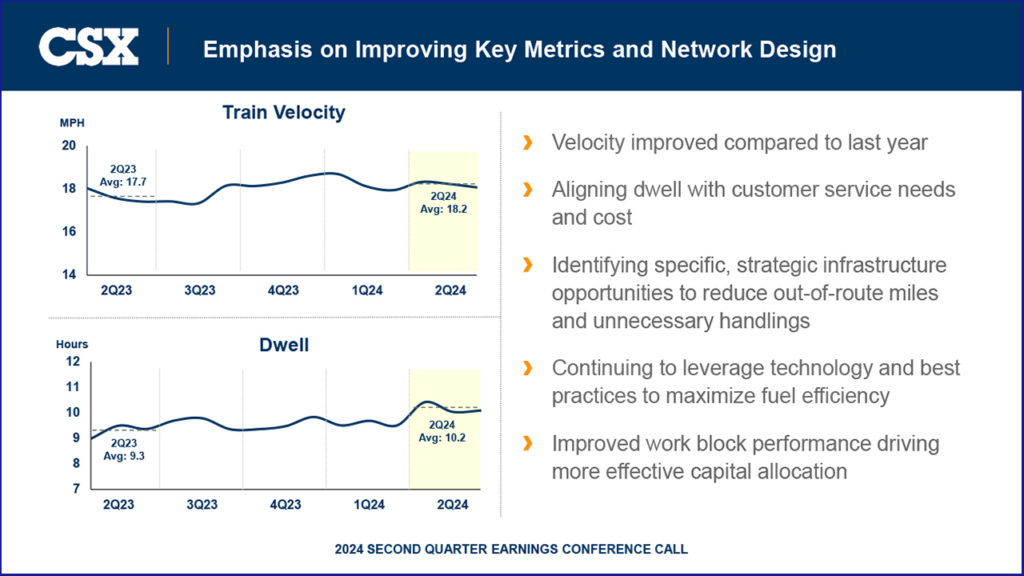

Network velocity improved compared 2Q23, as CSX is “aligning dwell with customer service needs and cost, “identifying specific, strategic infrastructure opportunities to reduce out-of-route miles and unnecessary handlings and continuing to leverage technology and best practices to maximize fuel efficiency,” Cory said. “Improved work block performance is driving more effective capital allocation.”

Second-quarter Merchandise revenue and volume grew 5% to $2.3 billion and 1% to 683,000 units, respectively, compared to the prior-year period. Executive Vice President and Chief Commercial Officer Kevin Boone said 2H24 expectations include “Merchandise volume sustained by ramping of business wins, customer engagement and strong operational execution. Positive market trends are supporting Chemicals, Forest Products, and Ag & Food. Strong Southeast infrastructure activity and accelerating industrial development are driving strength in Minerals. Metals likely be challenged by soft steel pricing and plentiful inventories. We are pricing above inflation but reflective of shifting mix dynamics.”

Second-quarter Intermodal revenue and volume grew 3% to $506 million and 5% to716,000 units, respectively, compared to the prior-year period. In 2H24, international intermodal “is expected to stabilize, supported by strong import activity and favorable partnerships,” Cory said. “There is a potential for modest domestic intermodal improvement, benefiting from incremental modal conversions, expanding partnerships and new lane offerings, but persistently weak trucking markets continue to cap the near-term pricing upside.”

Coal is a different story. Revenue dropped 12% to $563 million, and volume fell 3% to 179,000 units, compared to 1Q23. Yet, “export coal volumes were supported by strong operational flexibility and steady demand, and Curtis Bay becoming fully operational at the end of May,” Corey said. “Our export pricing is reflective of a modest easing of global benchmarks. Domestic coal is somewhat tempered by low natural gas prices but is gaining modest support from rising power consumption.”

TD COWEN INSIGHT: CSX MANAGING WELL THROUGH UNCERTAIN TIMES

By Jason Seidl, Elliot Alper and Uday Khanapurkar

CSX came above our forecast and consensus expectations in 2Q24 and reiterated its financial outlook for the full year. The first-half OR improvement was largely expected given favorable comparisons. CSX continues to manage costs amid multiple headwinds into 3Q24. We modestly lower our estimates to be more conservative, and our $36 PT remains intact.

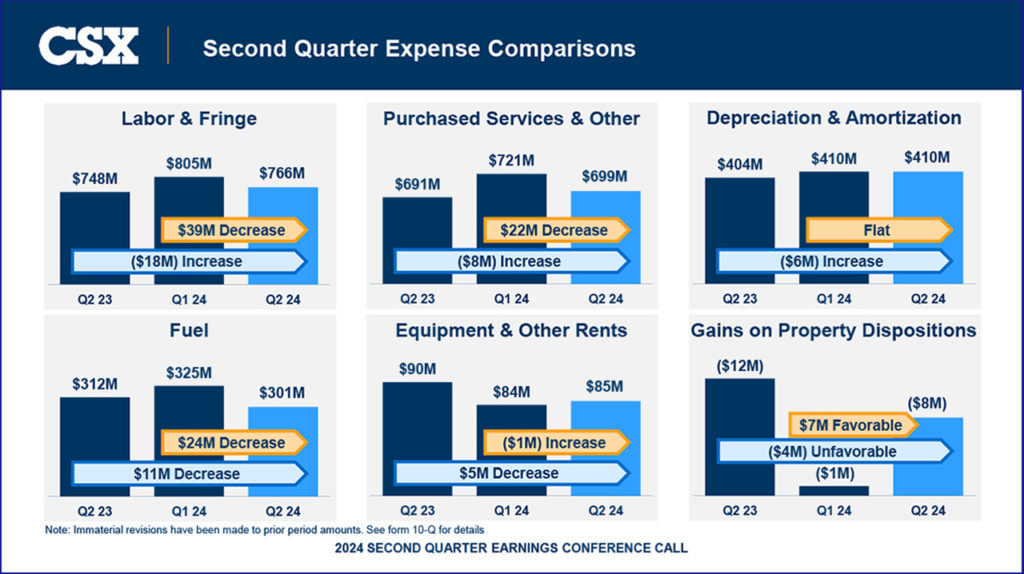

CSX’s reported 2Q EPS of $0.49 beat our $0.47 estimate and Street estimate of $0.48. Consolidated revenues of $3.7 billion were about in line with our estimates. The adjusted OR of 60.9% beat our projection by 160bps. A previously disclosed accounting change did not impact 2Q24 in a material manner, though 2Q23 expenses were revised up, affecting y/y comps slightly.

Coal RPU headwinds are expected to pressure margins in 3Q24, offsetting a relatively better demand picture. Soft domestic volumes due to substitution to natural gas drove carloads down 3% y/y, though export volumes grew 8% y/y with the Curtis Bay facility fully operational at the end of May following restored operations at the Port of Baltimore. We model coal RPU down MSD (moving standard deviation) sequentially in 3Q24, in line with CSX’s guidance.

Merchandise was a bright spot in the quarter with revenue per carload up 4% y/y as CSX extracted inflation-plus pricing on carloads up 1% y/y. CSX saw positive trends in chemicals and forest products. Industrial development momentum remains considerable per management, which we found encouraging, given some transports have pointed to hiccups in infrastructure-related volumes. CSX credited industrial strength in the Southeast to the momentum while highlighting that many relatively small projects are driving growth.

Overall, management expects low- to mid-single-digit volume and revenue growth in the back half of the year, and now expects “meaningful improvement” in OR in 2H24. CSX did not quantify the magnitude of improvement, though sequential puts/takes leads us to model modest sequential OR deterioration for 3Q24. New labor contracts effective July 1 will create a cost headwind that management works to offset with costs it can control, and OR may ultimately hinge on carloadings through the remainder of the quarter, which currently sit at +1.9% QTD according to the data we track. CSX had the benefit of hearing most other transports report 2Q earnings, and sounded marginally more cautious on the demand environment vs. 1Q, in our view.

CSX has not seen material signs of import volumes translating to domestic business yet, though we believe this could intensify in the coming months if restocking demand holds steady. Management struck a somewhat cautious tone at times on general macroeconomic confidence, notwithstanding the recent scare in financial markets. In contrast to merchandise pricing, intermodal rates are expected to see continued pressure into next year. Indeed, we do not expect an intermodal rate recovery until 2H25 at the earliest, given current OTR trends/commentary.

We lower our 2024 and 2025 EPS estimates to $1.94 from $1.98 and $2.15 from $2.20, respectively. Continuing to use our 16.5x multiple, our price target of $36 remains intact.

CSX is a high-quality company with solid fundamentals that appears well-positioned to benefit from long-term economic growth. Our base case assumptions: Rail volume recovery picks up as inventory restocking resumes, and CSX maintains its ability to command solid pricing. Our upside scenario: Global demand for U.S. coal picks up, and truckload capacity tightens, thereby allowing the railroads to raise prices on their intermodal product. Service improvements pick up pace. Forthcoming catalysts: Long-term intermodal growth to be driven by the ongoing shift from the highway as well as expansion of some of the company’s hubs, and potential longer-term benefits from the ongoing operational turnaround plan. Our downside scenario: Rail volume recovery is delayed, and truckload capacity remains materially elevated.