“Easing inflation, early-year warehouse tightening, a resilient supply chain job market, and shifting import behavior as frontloading fades” are among the highlights of ITS Logistics’ February 2026 Supply Chain Report. The strike down of POTUS 47 tariffs by the U.S. Supreme Court, it noted, has “significant implications for the global market.”

“January import volumes signaled a potential return to normalized behavior—only to be disrupted by the latest rulings on global tariffs,” ITS Logistics, a Nevada-based third-party logistics (3PL) firm, reported Feb. 26. “Trucking capacity remains unseasonably tight, and warehousing has shifted rapidly from post-holiday softness to early-cycle tightening. Despite downward revisions to 2025 job numbers, January’s labor market was unexpectedly strong, though consumer sentiment in the overall economy continues to decline.”

The U.S. Supreme Court on Feb. 20 struck down POTUS 47’s IEEPA tariffs, resulting in the U.S. Customs and Border Protection agency halting duty collections and deactivating all tariff codes as of Feb. 24, according to ITS Logistics. “Immediately following the ruling, [POTUS 47] announced he would be implementing a blanket 10% tariff under Section 122 of the 1974 Trade Act, which allows the President to enact ‘temporary import surcharges’ without Congressional approval for up to 150 days,” the 3PL firm said. “The new so-called global tariffs went into effect on Feb. 24, and the White House stated it is working on a formal order to increase the rate to 15%. The fresh wave of geopolitical uncertainty forces shippers to reevaluate their sourcing strategies following months of large-scale shifts in global supply chain trends.”

“Similar to mid-year 2025, we will likely see a split in behavior between shippers who repeat frontloading activity to seize potential cost-saving opportunities and those who pause and wait for clarity in the coming months,” ITS Logistics Chief Commercial Officer Josh Allen said. “This stop-and-go supply chain traffic will contribute to ongoing volatility. As it relates to warehousing, this month’s report shows conditions shifted quickly from post-holiday softness to early tightening in January, as inventory drawdowns reversed and utilization rebounded into expansion territory. While excess capacity was briefly absorbed faster than typical seasonal patterns, warehousing prices and inventory carrying costs remained firmly expansionary, highlighting persistent structural cost pressure across the sector.”

As the industry looks ahead, ITS Logistics reported, expectations point to “continued pricing pressure and constrained capacity growth.” Despite marginal cooling in mid-February for the trucking sector, it continued, “capacity remains unseasonably tight, with volumes and rates significantly above recent historical averages in both the dry van and reefer markets.”

Noted Allen: “Newly announced non-domiciled restrictions will continue to place strain on the capacity pool over the coming months, converging with peak produce seasons and likely downstream effects from the new global tariffs ruling.”

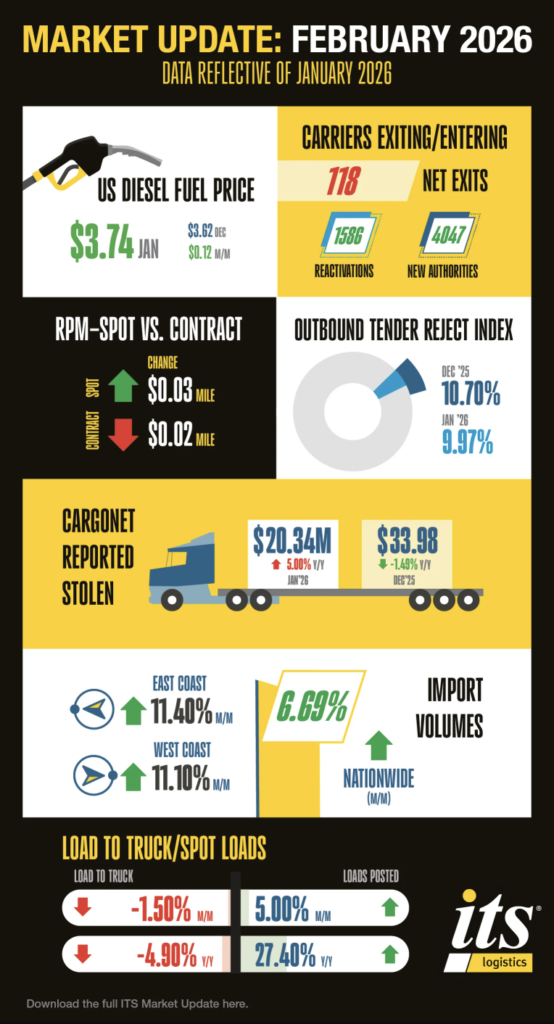

The report also highlighted that U.S. container import volumes totaled 2,318,722 TEUs (Twenty-Foot Equivalent Units) in January. While down 6.8% year over year, ITS Logistics said, this was “slightly above” the six-year average for the month and posted “modest gains” from December. The early-year dip in U.S. container import volumes, it added, “may indicate that import behavior is returning to normal after a year disrupted by frontloading.”

Concerning the nation’s economy, in January 2026 the U.S. economy “maintained steady momentum as inflation continued to ease, with headline and core measures cooling to their lowest levels in months,” according to ITS Logistics.

“The labor market saw stronger than expected job gains and a stable unemployment rate offset by signs of softer underlying momentum and sector specific weakness,” said Josh Allen. “Consumers demonstrated mixed behavior, and spending held up. However, confidence fell sharply amid lingering concerns about jobs and prices. While January showed resilience, overall momentum remained moderate and uneven across sectors. Employers added about 130,000 jobs, well above the consensus expectations, and the unemployment rate decreased to 4.3% from 4.4% in December 2025.”

Last December, in a 2026 supply chain employment projection, Supply Chain 24/7 reported that “companies need to focus as much on developing their people as they do on adopting new technology in this current AI-driven environment,” according to ITS Logistics. “As more schools offer supply chain programs with strong admission rates for students with the necessary academic attributes, turnover in the industry continues to add to the strain. A survey found an average turnover rate of 11.6%, with only about one in five participants reporting no departures.” ITS Logistics noted that the Bureau of Labor Statistics projects 17% employment growth for logisticians from 2024 to 2034, which is “almost five times faster than the average for all occupations” and equates to approximately 26,400 job openings annually between new positions and replacement hiring as professionals retire or change careers.

Separately, ITS Logistics recently released its February 2026 US Port/Rail Ramp Freight Index, which identified a “return to seasonal Lunar New Year demand patterns layered over weather and regulatory-related disruption impacting inland transportation.” While overall port and rail ramp operations remained at normal levels, it noted, “downstream rail and trucking networks are facing elevated concern in select regions.”

Further Reading:

- ITS Logistics Publishes January U.S. Port/Rail Ramp Freight Index

- ITS Logistics Issues December Supply Chain Report

- ITS Logistics Publishes November Supply Chain Report

- ITS Logistics Issues November US Port/Rail Ramp Freight Index

- ITS Logistics Issues October US Port/Rail Ramp Freight Index

- ITS Logistics Releases September Supply Chain Report

- ITS Logistics Publishes September US Port/Rail Ramp Freight Index

- ITS Logistics Issues August Supply Chain Report

- ITS Logistics Releases August US Port/Rail Ramp Freight Index

- ITS Logistics Publishes July Supply Chain Report

- ITS Logistics Issues July US Port/Rail Ramp Freight Index