After Norfolk Southern prevailed in its hard-fought proxy fight victory earlier this year, we wrote that “as Norfolk Southern finally pulls out of the station, leaving its activist detractors shouting on the side of the tracks, the future is promising under CEO Alan Shaw … for greater operational efficiency and productivity.”

In the days afterward, we heard from countless investors, railroaders and media commentators. While virtually all expressed relief that the activist did not prevail, some thought we were too sanguine in our belief that Norfolk Southern would actually deliver on the lofty promises made during the heat of the proxy fight.

Indeed, the baseline expectation among many investors and analysts seemed to be that the railroad would never be able to pull off the aggressive turnaround it promised, unable to slay the dragons of bloated operational inefficiency, safety woes, and loss of market share that resulted in Norfolk Southern underperforming peer railroads for years.

In this case, it did not pay to be cynical—with the triumphant release of the second-quarter 2024 earnings report, the first since the proxy fight win, and an immediate 10% surge in stock price, surprising some analysts and serving as strong evidence that Norfolk Southern’s turnaround is gaining speed and momentum, as we’d presciently written.

Of course, it is far too early to declare victory, and it is still early innings; but Norfolk Southern delivered impressively on its single most important mandate from shareholders, driving a 5% quarter-over-quarter improvement in its all-important operating ratio (OR), while reiterating guidance for continued aggressive OR improvements moving forward.

But even more important, some single-minded financial analysts do not appreciate the fact Norfolk Southern is driving productivity gains the hard (but right) way, not through reckless slash-and-burn, or mass layoffs, but the result of bona fide network improvements across virtually every measure: increased car-miles per day, increased train speed, and reduced terminal dwell. As a result, unlike prior turnarounds at peer railroads which resulted in service quality deterioration, furious customers switching from rail to truck and shrinking volumes, Norfolk Southern has driven a virtuous flywheel effect where productivity gains enhance rather than detract from service quality and safety.

Remarkably, despite the freight recession, Norfolk Southern managed to seize significant market share from rail and more impressively, truck competitors for the first time in years, growing intermodal volumes 8% and carload volumes by 7%, far outpacing all peers. One analyst noted that there is a “long list” of customers newly eager to switch back to rail from truck thanks to Norfolk Southern’s “vast improvements,” positioning the railroad well for much more high-margin merchandise volume gains to come in future quarters. No wonder Norfolk Southern’s stock surge was one of the few bright spots amidst an otherwise bloody earnings season for a battered transports sector.

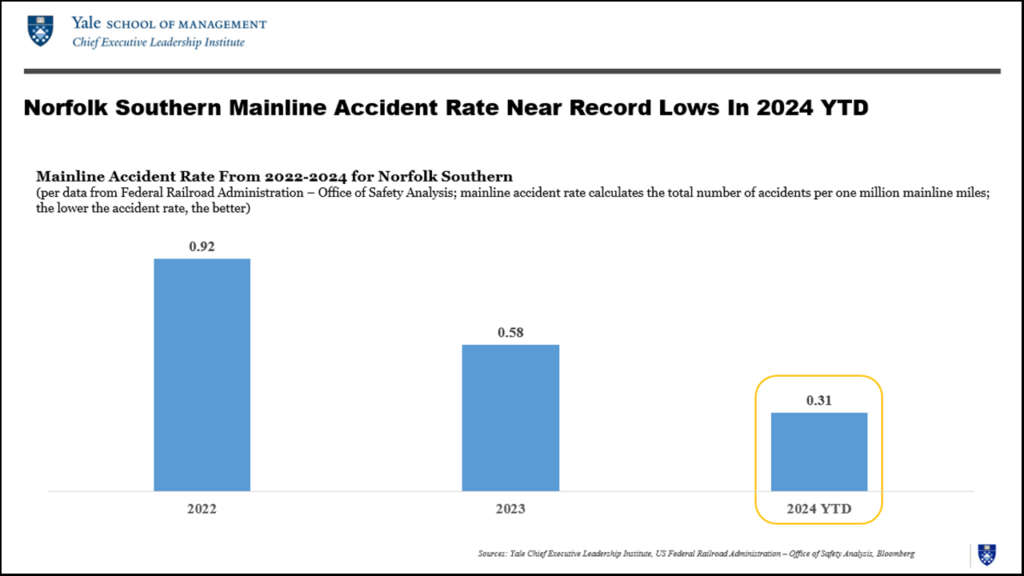

Similarly, Norfolk Southern’s genuine network improvements in lieu of the more common alternative—mindless cost-cutting—have buttressed safety, resulting in a near-record low accident rate, 50% lower than last year’s rate and 70% lower than 2022. It is hard not to be impressed by the sui generis personal commitment CEO Alan Shaw has made toward delivering on his safety promises, which time has demonstrated to be heartfelt and genuine. Whereas many other CEOs would have hidden behind layers of hired PR flaks and resorted to carefully scripted “damage control,” Shaw visited East Palestine, Ohio, the site of the tragic derailment, established enduring personal relationships of mutual trust with countless local community members, cooperated extensively with NTSB investigators with excruciating honesty, and deeply feels the weight of his safety promises, believing it a matter of his personal integrity.

The fact that this virtuous flywheel is already paying off—where productivity gains done the right way have driven safety improvements and the best service product delivered to customers in years—reaffirms that the vast majority of shareholders who voted overwhelmingly for Alan Shaw to remain as CEO made the right decision. Few new CEOs in any industry have had to navigate a more eventful first two years than Shaw, who has fought—and won—more uphill battles than most CEOs have to deal with across their entire tenures. With his leadership credibility now forged through fire, even Shaw’s critics readily concede that he has grown appreciably on the job, and he is now widely seen as one of the most widely admired rail executives operating today.

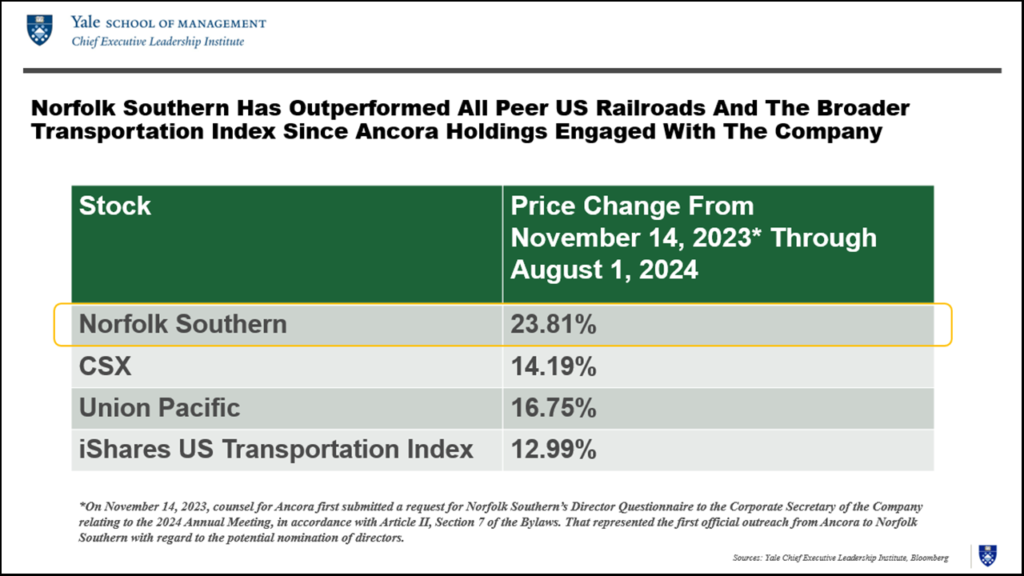

Of course, Shaw is supported by a strong team, including Chief Operating Officer John Orr and Chief Marketing Officer Ed Elkins, and Norfolk Southern has a strong board with rail expertise, led by Chair Claude Mongeau. But not to be overlooked is the commendable engaged shareholder role played by the activist firm Ancora Holdings, which remains a shareholder, is led by respected Cleveland philanthropist Fred DiSanto—and had three experienced, highly qualified members elected to the NS board: Gil Lamphere, Sameh Fahmy and William Clyburn, Jr. The financial outperformance of Norfolk Southern stock since Ancora first reached out to the company last year is remarkable, with the stock far outperforming all peer U.S. Class I railroads and the broader transportation index under CEO Alan Shaw’s brilliant leadership.

While we, like many others, were confounded by some of Jim Chadwick’s needlessly unfortunate tactics and unrealistic approach during the proxy fight, nevertheless, at a minimum, Ancora Holdings deserves tremendous credit for raising heightened awareness about Norfolk Southern’s potential within the investment community, which has helped light a fire under company leadership to turbocharge planned improvements and increase shareholder engagement. It is hard to believe any rational shareholder would want to wage a proxy fight next year, as long as the company continues to deliver such strong financial and operational performance, and especially if shareholder returns become an increasingly important focus of capital allocation priorities over time, as many analysts expect it will once the industry emerges from the cyclical downturn.

More than a century ago, as he examined the dilapidated Kansas City Southern network, pioneering rail executive Leonor F. Loree famously exclaimed, “This is a helluva way to run a railroad!” Now, the right way to run a railroad is being modeled by Alan Shaw at Norfolk Southern, as NS continues pulling out of the station going full speed ahead, delivering on its promises to shareholders and proving its critics wrong.

Jeffrey Sonnenfeld (left) is the Lester Crown Professor in Management Practice and Founder and President of the Yale Chief Executive Leadership Institute at the Yale School of Management. Steven Tian is Director of Research at the Yale Chief Executive Leadership Institute and a former quantitative investment analyst with the Rockefeller Family Office.