NS: ‘Reliable Service, Measurable Safety Gains’ (UPDATED With TD Cowen Commentary, 1/30)

For fourth-quarter 2025, NS reported that revenue was $3.0 billion, income from railway operations was $937 million, operating ratio was 68.5%, and diluted earnings per share were $2.87.

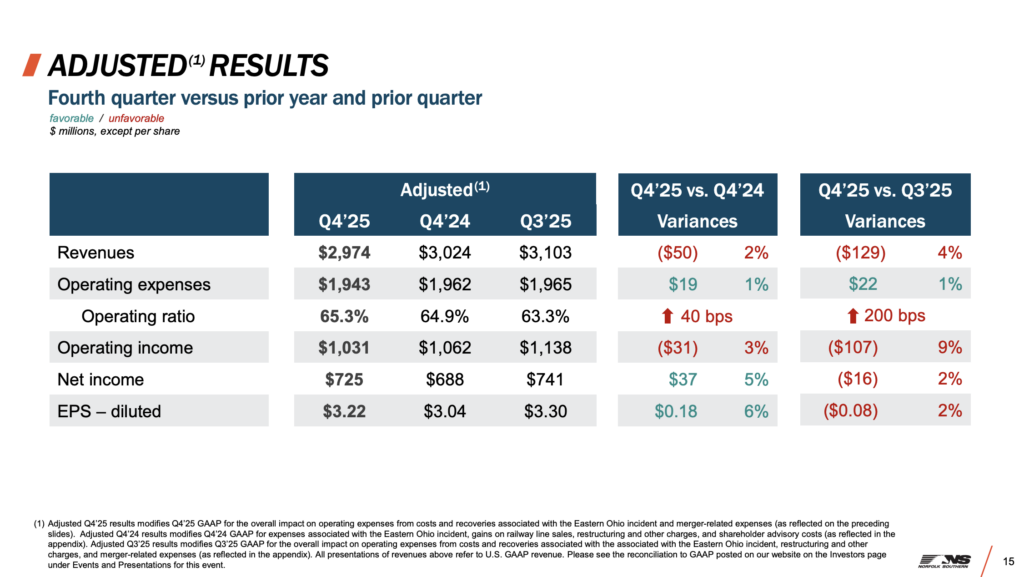

After adjusting the results to exclude merger-related expenses and the effects of the East Palestine, Ohio, derailment in 2023, fourth-quarter income from railway operations was $1.0 billion, the operating ratio was 65.3%, and diluted earnings per share were $3.22.

For fourth-quarter 2025, NS posted:

- Railway operating revenues of $3.0 billion, down $50 million, or 2%, compared to the fourth quarter 2024, on a volume decline of 4% year-over-year.

- Income from railway operations was $937 million, a decrease of $194 million, or 17%, compared to fourth quarter 2024 which included railway line sales of $53 million. Fourth quarter 2025 includes a large land sale that resulted in a net gain of $85 million.

- Adjusting for: the effects of the Eastern Ohio incident in both years; merger-related expenses in 2025; and gains on railway line sales in 2024, income from railway operations was $1.0 billion, down $31 million, or 3%, compared to adjusted fourth quarter 2024.

- Adjusting for: the effects of the Eastern Ohio incident in both years; merger-related expenses in 2025; and gains on railway line sales in 2024, income from railway operations was $1.0 billion, down $31 million, or 3%, compared to adjusted fourth quarter 2024.

- Operating ratio in the quarter was 68.5% compared to 62.6% in fourth quarter 2024 which included the aforementioned railway line sales.

- Adjusting for merger-related expenses and the effects of the Eastern Ohio incident, the operating ratio for the quarter was 65.3%.

- Adjusting for merger-related expenses and the effects of the Eastern Ohio incident, the operating ratio for the quarter was 65.3%.

- Diluted earnings per share were $2.87, down $0.36, or 11%, compared to fourth quarter 2024 which included the aforementioned railway line sales.

- Adjusting for merger-related expenses and the effects of the Eastern Ohio incident, diluted earnings per share were $3.22, up $0.18, or 6%, compared to adjusted fourth quarter 2024.

For full-year 2025, NS posted:

- Railway operating revenues of $12.2 billion, up $57 million, compared to full year 2024.

- Fuel surcharge revenue declined $134 million compared to 2024, which represents a 1% headwind to overall revenues.

- Fuel surcharge revenue declined $134 million compared to 2024, which represents a 1% headwind to overall revenues.

- Income from railway operations was $4.4 billion, an increase of $285 million, or 7%, compared to full year 2024.

- Adjusting for: the impact of merger-related expenses in 2025; restructuring and other charges in both years; the Eastern Ohio incident in both years; and gains on railway line sales in 2024, income from railway operations was $4.3 billion, up $122 million, or 3%, compared to adjusted 2024.

- Adjusting for: the impact of merger-related expenses in 2025; restructuring and other charges in both years; the Eastern Ohio incident in both years; and gains on railway line sales in 2024, income from railway operations was $4.3 billion, up $122 million, or 3%, compared to adjusted 2024.

- Operating ratio in 2025 was 64.2%, an improvement of 220 basis points, compared to 66.4% in 2024.

- Adjusting for the impact of merger-related expenses, restructuring and other charges, and the Eastern Ohio incident, the operating ratio for 2025 was 65.0%. This represents 80 basis points of improvement from adjusted 2024 which was 65.8%.

- Adjusting for the impact of merger-related expenses, restructuring and other charges, and the Eastern Ohio incident, the operating ratio for 2025 was 65.0%. This represents 80 basis points of improvement from adjusted 2024 which was 65.8%.

- Diluted earnings per share were $12.75, an increase of 10% compared to 2024.

- Adjusting for the impact of merger-related expenses, restructuring and other charges, and the Eastern Ohio incident, diluted earnings per share were $12.49, up $0.64, or 5%, compared to adjusted 2024.

“In the face of a volatile and challenging macro-economic backdrop, our team focused on the controllables—delivering outsized productivity savings in excess of $215 million that accompanies our safety and service improvements. As we move through 2026, the demand environment remains unclear, but we are steadfastly focused on prioritizing the safety of our employees and communities, delivering consistent customer service, and driving further productivity gains to contain our costs in any volume environment,” said George.

TD Cowen Commentary

NSC Focuses On Cost As Top Line Pressure Persists

By Jason H. Seidl (Wall Street Contributing Editor), Elliot Alper and Uday Khanapurkar

NSC modestly missed our forecast and consensus expectations in 4Q when adjusting for one-times. ’26 guidance focuses on cost as NSC faces demand and pricing pressures, management was not confident on top line growth to start the year. Investors focus on merger which should continue to backstop shares, expect refiling in March. $314 PT intact, reiterate Buy.

- 4Q adj. results included a gain on land sale and tax rate benefit excluding which adj. EPS ex-items of ~$2.65 missed our $2.75 and consensus of $2.76 by ~a dime. Consolidated top line was in line with our estimate but adj. OR ex-item was 68.2% which was 290bps worse than our forecast.

- Service metrics appeared robust in 4Q with headcount -1% Y/Y dropping slightly sequentially. Qualified T&E headcount was -7% Y/Y in 4Q within this. Fuel efficiency improvements continued in 4Q, +4% Y/Y. Broad productivity tailwinds mitigated impacts from soft network throughput. Encouraging service improvements allowed mgmt. to underwrite a $100MM increase in opex savings for 2026. This should modestly mitigate inflationary pressures but NSC’s opex guide for 2026 nonetheless implies a level above our pre-print estimate on inflationary pressures and land sale normalization even as top line expectations remain anchored in relatively soft territory (weak imports, industrial trends). Mgmt. also sees capex -14% in 2026, again citing productivity. Given imperative to preserve service quality through the ongoing merger review process, we believe a lowered capex guide signals confidence in the sustainability/structural nature of service efforts/improvements.

- 4Q carloads -4% was driven by well-understood competitive share shift in intermodal which should persist through 3Q26 (when NSC laps the 1pt headwind) as merger review resolution is a mid ’27 story at best. The broader market is not expected to provide much support with international outlook dampened by tariff overhang. Coal should see some demand uptick near-term with utility/domestic strong but mgmt. did not suggest any catalysts to yields and export tons. Broader industrial end-market outlook was soft in concurrence with transports that have reported EPS thus far. We continue to model LSD top line growth for the year.