“Our back-to-basics approach continues to drive strong results,” CN President and CEO Tracy Robinson said during the Class I’s third-quarter financial report on Oct. 25. “We have a busy fourth quarter, with a strong start in the Canadian grain crop, and we are resourced for the months ahead. We are pleased to be raising our 2022 outlook to reflect our performance.”

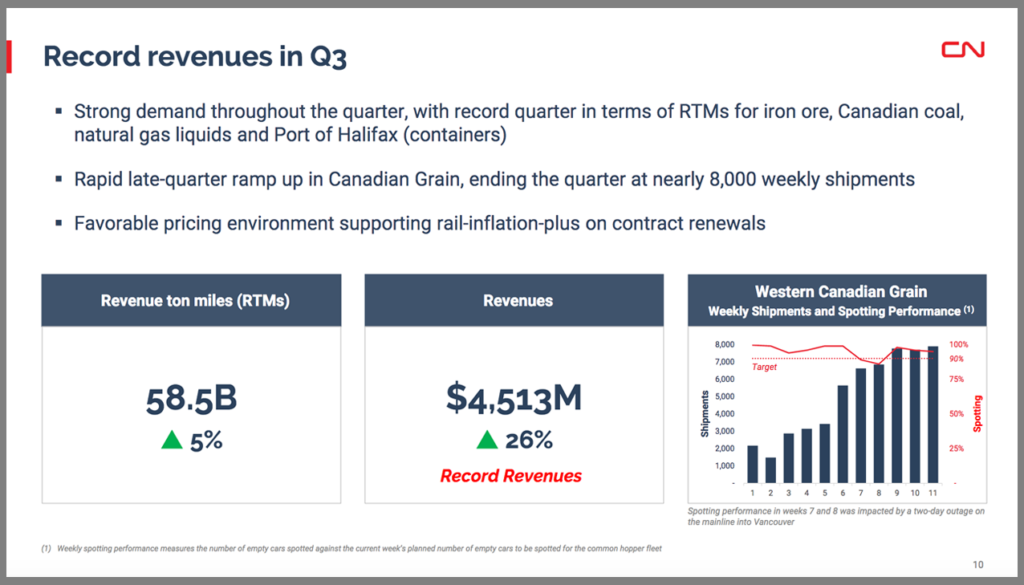

CN on Oct. 25 reported “record” revenues of C4.513 billion for the three-months ended Sept. 30, 2022, up 26% (an increase of C$922 million) from the prior-year period. “The increase was mainly due to higher fuel surcharge revenue driven by higher fuel prices, freight rate increases, higher Canadian export volumes of coal via west coast ports, higher volumes of U.S. grain, and the positive translation impact of a weaker Canadian dollar,” according to the railroad.

Revenue ton miles (RTMs), measuring the weight and distance of freight transported by CN, were up 5% from third-quarter 2021. Freight revenue per RTM was up 22% compared to the year-earlier period. This was “mainly driven by higher fuel surcharge revenue driven by higher fuel prices, freight rate increases and the positive translation impact of a weaker Canadian dollar,” the railroad said.

Operating expenses for third-quarter 2022 grew 15% to C$2.581 billion. CN said this was“mainly driven by higher fuel prices and the negative translation impact of a weaker Canadian dollar; partly offset by Transaction-related costs of $84 million recorded in the third quarter of 2021 resulting from the terminated CN Merger Agreement with Kansas City Southern.”

CN reported “record” operating income of C$1.932 billion, an increase of 44%, or an increase of 31% on an adjusted basis, which includes a C$47 million wage accrual for the tentative agreement reached with U.S. unions, vs. third-quarter 2021.

Diluted EPS came in at C$2.13, a decrease of 10%, which CN said was “mainly due to a merger termination fee received in the third quarter of 2021.” Diluted EPS was up 40% on an adjusted basis, which represents a quarterly record, the railroad noted.

Operating ratio, defined as operating expenses as a percentage of revenues, for third-quarter 2022 was 57.2%, an improvement of 5.5-points, or an improvement of 1.8-points on an adjusted basis, CN reported.

For the three-months ended Sept. 30, 2022, car velocity of 212 miles per day improved by 5%—the highest level since third-quarter 2016, CN reported—and dwell improved by 9% over the same period last year. Additionally, fuel efficiency improved by 1% to 0.838 U.S. gallons of locomotive fuel consumed per 1,000 gross ton-miles (GTMs), and origin train performance averaged 87%, an improvement of 12% compared with 78% for the same period in 2021.

2022 Outlook

Looking ahead, CN said it is now expecting to deliver in 2022 approximately 25% of adjusted diluted EPS growth vs. its April 26, 2022 target of 15%-20%, and free cash flow of approximately C$4.2 billion vs. its April 26, 2022 target range of C$3.7 billion to C$4.0 billion. Additionally, the railroad said it continues to target an operating ratio below 60% and a ROIC of approximately 15% in 2022. It is “assuming full-year low single-digit volume growth (RTMs).”

For more details, visit the CN Investors webpage.

The Cowen Insight: ‘Bulking Up the Bottom Line’

“CN’s third quarter came in above consensus expectations as the company’s bulk segment supported volumes, leading management to raise its full-year guidance,” reported Cowen and Company Managing Director and Railway Age Wall Street Contributing Editor Jason Seidl. “We modestly adjust our volume assumptions given our previous above-guidance estimate while adjusting for FX. We believe bulk volumes offer an inelastic tailwind into 2023 that position CN well ahead of an uncertain macro picture. Price target to $119.”

Key Cowen Takeaways:

• “CN recorded a top- and bottom-line beat with third-quarter adjusted EPS of $2.13 CAD exceeding the Street forecast of $2.01 CAD and our estimate. Third-quarter adjusted operating ratio (OR) of 57.2% came in better than expectations improving 180 bps year-over-year (y/y) on robust pricing, volumes and a favorable fuel surcharge lag.

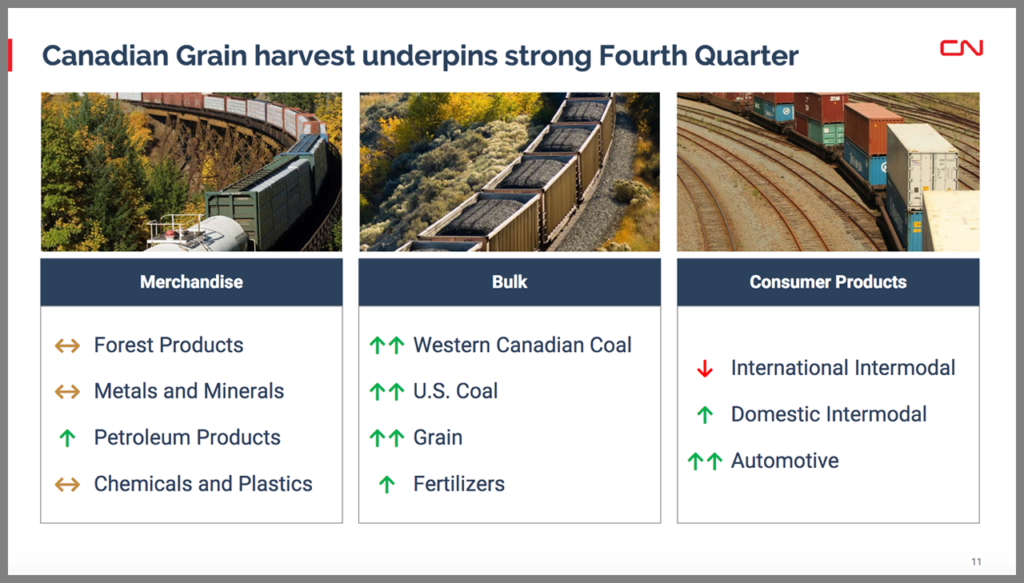

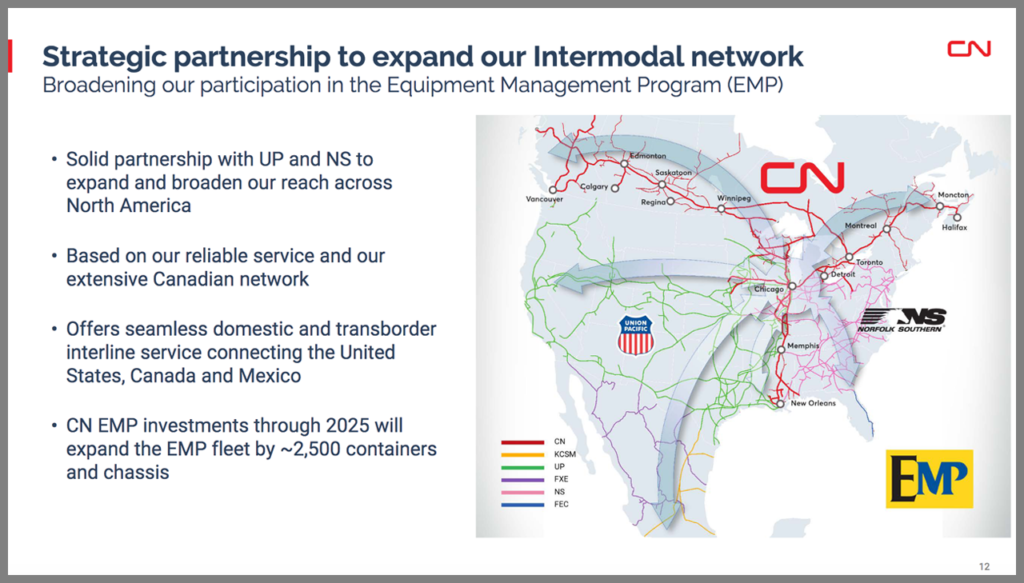

• “Volumes remained very solid in the third quarter growing 2.9% y/y due to a bumper Canadian grain harvest and tailwinds to coal and fertilizer volumes generated by the war in Ukraine. These tailwinds should persist in the fourth quarter and into 2023, propping up volumes. Low water levels in the Mississippi should also support volumes for a while as the CN network is positioned to take freight off the Mississippi. CN also expects a boost to volumes from participation in the Equipment Management Program (EMP) in partnership with Union Pacific and Norfolk Southern. We were encouraged to hear that container volumes at the Halifax facility were up over 20% indicating healthy demand for the resources deployed there, given management’s emphasis on the port on their second-quarter call. International intermodal volumes were a weak point in the third quarter declining 1.2% y/y and may be foreshadowing softness on the consumer side. Chemicals are also reportedly showing early signs of softness. Tailwinds should prevail in our view, and we take our fourth-quarter volume assumptions up to reflect this. Management appeared confident that volumes would remain strong irrespective of the economic outlook due to these unique tailwinds.

• “Strong yield growth of 23.8% y/y supported results this quarter but will likely step down in the fourth quarter and into 2023. Management reiterated commitment to pricing above inflation and emphasized that a third of the book is repriced annually. Given the inelastic nature of the tailwinds on the bulk side, we modestly adjust our fourth-quarter and 2023 pricing assumptions upward.

• “Management raised full year EPS growth guidance to approximately 25% from 15%-20%, and we come in on the high end of guidance at 27%. CN also reiterated their 2022 OR target of below 60%, which is very achievable in our view given the quality of volumes, healthy service metrics and a more manageable cost impact from labor negotiations.

• “We adjust our 2022 and 2023 EPS estimates to $5.74 USD from $5.65 USD and $6.25 from $6.20, respectively. Continuing to use our 19x multiple (which we brought down earlier in October to be more in line with its historical average) and our new 2023 EPS estimate, our price target increases by $1 to $119 USD. We believe CN’s bulk segment exposure (Western Canadian coal, U.S. coal, grain, and fertilizers) positions the company well into 2023, as its inelastic segments should provide support amid potential consumer softness.”