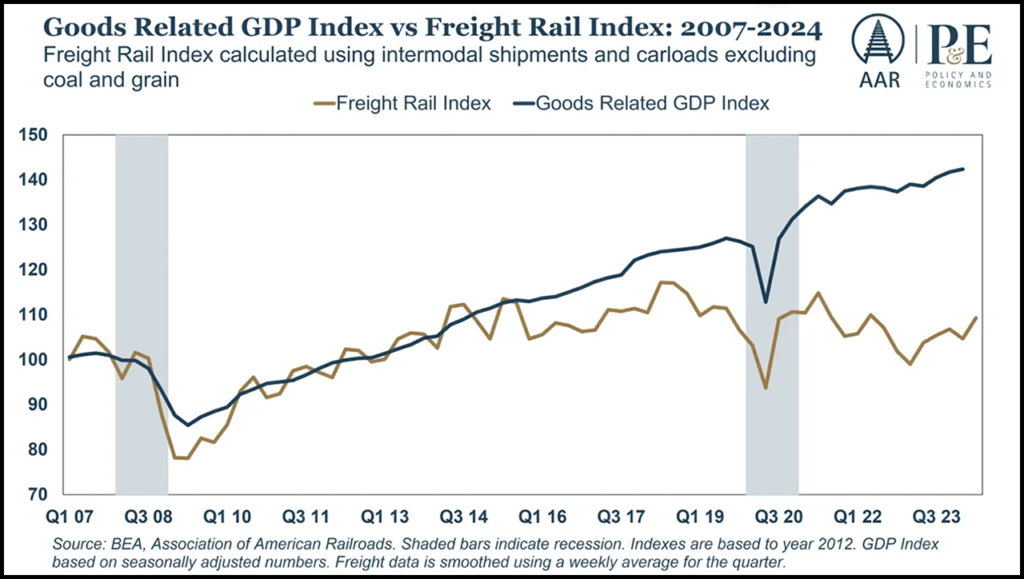

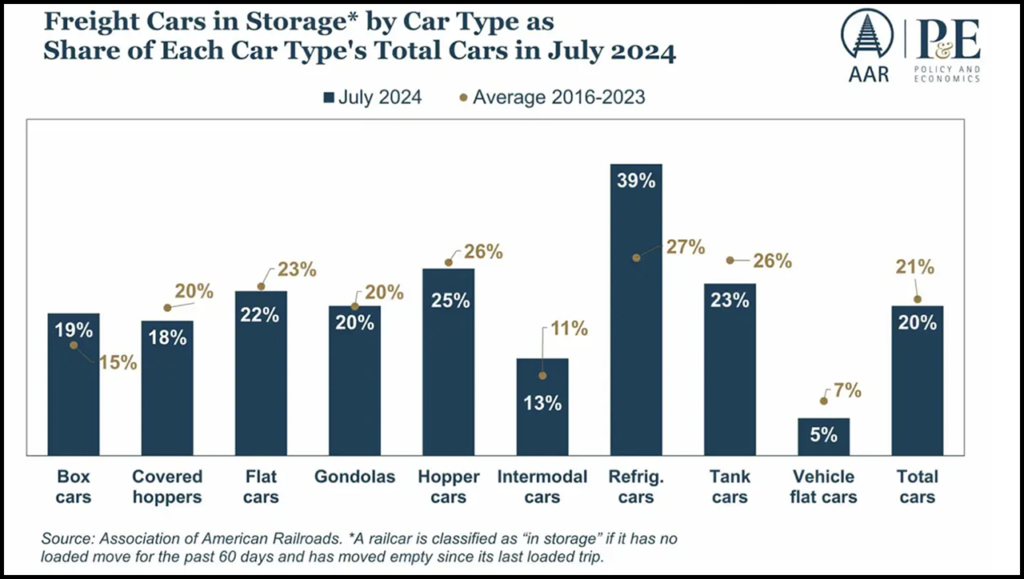

As part of Rail Industry Overview, AAR is debuting the Freight Rail Index, which “tracks movement across the most economically sensitive rail traffic commodities.” According to the association, the index includes intermodal and carloads but excludes coal and grain, whose volumes are driven by factors like weather or transitions in energy markets that are less directly linked to macroeconomic activity. “Historical data shows that freight activity, measured by the Freight Rail Index, and Gross Domestic Product (GDP) tend to rise and fall in tandem, making the Freight Rail Index a useful barometer for the economy,” AAR reported.

Key takeaways from the first edition of Rail Industry Outlook (July 2024; scroll down to download) include:

- “June rail data, closely tied to economic performance, suggests a cautiously optimistic outlook for economic growth amid prevailing uncertainty. Potential interest rate cuts later in 2024 or early 2025 are expected to stimulate industrial output, which has historically driven growth in rail carload volumes across key commodities.”

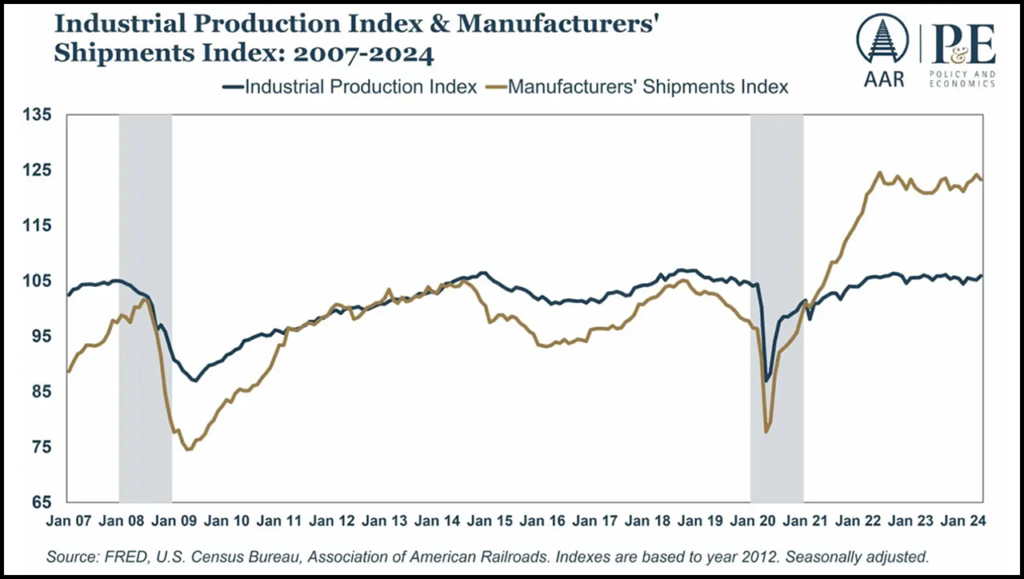

- “Recent data indicating an uptick in industrial output brings a beacon of hope, hinting at a possible end to the prolonged manufacturing slowdown. If this activity continues, rail volumes for raw materials and finished goods are likely to follow.”

- “Intermodal transport continues to shine, fueled by robust consumer demand. This sector’s sustained growth is essential for maintaining overall economic momentum, particularly in the retail sector.”

“The trajectory of rail traffic volumes for the rest of 2024 will heavily depend on the pace of economic growth, influenced by job market performance, inflation rates and the Federal Reserve’s monetary policies,” the AAR Policy and Economics Department wrote in the July edition of Rail Industry Overview. “Despite a sharp decline from their peak in June 2022, both the consumer price index (CPI) and the Fed’s preferred inflation measure—the price index for personal consumption expenditures—remain above the Fed’s 2% target and have recently plateaued. Rising raw material costs continue to challenge suppliers, impacting manufacturers and the overall supply chain. For railroads, lower overall inflation could lead to higher consumer confidence, increased demand for goods and a greater need for shipping services. It also means more predictable and manageable input costs, providing a more stable environment for long-term planning.”

“Rail traffic data is among the richest, most timely economic data in the U.S.,” said AAR Chief Economist Rand Ghayad during the July 8 announcement of Rail Industry Overview. “Whether it is housing, energy markets or consumer spending, rail traffic touches them all. At a time when various indicators suggest very different paths ahead for the economy, rail traffic data is a common thread that can help connect the dots. Amid prevailing uncertainty, June rail data gives reason for cautious optimism about the road ahead. Continued strength in intermodal traffic and modest growth across key carloads suggest that consumer spending remains robust for now and the prolonged manufacturing slowdown may be coming to an end.”

To view Rail Industry Overview reports each month, visit the AAR website or subscribe by clicking here.

For a deeper dive into rail traffic data, subscribe to AAR’s Rail Time Indicators report. Previously produced monthly, it is now a quarterly rail traffic and economic commentary. The first part covers U.S., Canadian, and Mexican freight rail traffic, containing tables and charts for recent months and the year to date; data cover intermodal and 20 carload commodity categories. The second part includes charts and data on macroeconomic indicators, such as GDP, housing, industrial production and employment.

AAR also releases its Weekly Railroad Traffic Report. For the latest edition, with June 2024 and week ending June 29, 2024, data, read “AAR: Rail Traffic ‘Balanced’ Through June.”

For a list of and to subscribe to all AAR publications, click here.